One Nation – One TAX

iProGST

Adept is developing a comprehensive software on GST – iPro.GST

Our domain knowledge on MCA compliances, Taxation and various other applications led by a powerful professional team will ensure to deliver a world class software to enable smooth and accurate filling – and above all ON TIME. We will keep you updated on the latest rules and drafts, as and when introduced by Government of India. We will notify you on launch of our software and be happy to showcase the product to all at an earliest date.

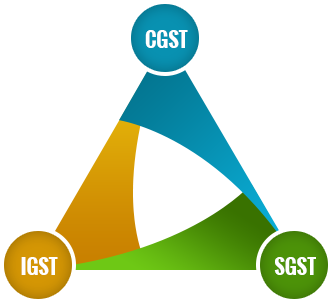

- IGST stands for Central GST

- This is applicable on interstate and import transactions

- Tax collected is shared between Centre and State

- CGST stands for Central GST

- This is applicable on supplies within the State

- Tax collected will be shared to Centre & State

- SGST stands for Central GST

- This is applicable on supplies within the State

- Tax collected will be shared to Centre & State

Taxes Subsumed

The taxes which will get subsumed under GST are

| Subsumed in GST | Not subsumed in GST |

|---|---|

| Central Excise | Basic Customs duty |

| Service Tax | Alcohol for human consumption |

| VAT / Sales Tax (CST) | Petrol / Diesel / Aviation fuel / Natural Gas* |

| Entertainment Tax | Stamp duty and Property tax |

| Luxury Tax | Toll tax |

| Taxes on lottery | Electricity Duty |

| Octroi | |

| Purchase tax | |

| Entry Tax |

Registration Threshold Limit

Regular Dealer

North East India |

Aggregate Turnover exceeds | 9L for Registration | 10L for Payment of Tax |

Rest of India |

Aggregate Turnover exceeds | 19L for Registration | 20L for Payment of Tax |

COMPOSITE DEALER

Composition Levy |

Aggregate Turnover exceeds | 9L for Registration |

Input Credit Adjustment

Proposed Returns

| Product | No. of companies | Type | Version |

|---|---|---|---|

| 1 | GSTR 1 | Upload all Outward supplies made by a taxpayer (other than compounding taxpayer and ISD) | By 10th of the month |

| 2 | GSTR-2A | Auto-populated details of inward supplies made available to the recipient on the basis of Form GSTR-1 furnished by the supplier | On 11th of the month |

| 3 | GSTR 2 | Addition (Claims) or modification in Form GSTR-2A should be submitted in Form GSTR-2 (other than a compounding taxpayer and ISD) | By 15th of the month |

| 4 | GSTR-1A | Details of outward supplies as added, corrected or deleted by the recipient in Form GSTR-2 will be made available to supplier | On 20th of the month |

| 5 | GSTR 3 | Monthly return TO BE Submitted- the auto-populated GSTR-3 (other than compounding taxpayer and ISD ) | By 20th of the month |

| 6 | GSTR-4A | Details of inward supplies made available to the recipient registered under composition scheme on the basis of Form GSTR-1 furnished by the supplier | Quarterly |

| 7 | GSTR 4 | Quarterly return for compounding. This includes auto-populated details from Form GSTR-4A, tax payable and payment of tax | By 18th of the month |

| 8 | GSTR-5 | Return by Non-Resident Taxable Persons (Foreigners) | Last day of registration |

| 9 | GSTR 6 | Return for Input Service Distributor (ISD) | By 15th of the month |

| 10 | GSTR-7 | Return for Tax Deducted at Source (TDS) | By 10th of the month |

| 11 | GSTR 8 | Statement of E-Commerce Operators | By 31st December of next FY |

| 12 | GSTR-9 | Annual Return – furnish the details of ITC availed and GST paid which includes local, interstate and import/exports | By 31st December of next FY |

| 11 | GSTR 9A | Furnish the consolidated details of quarterly returns filed along with tax payment details | By 31st December of next FY |

Law, Rules & Formats in GST

- Draft GST Registration Rules

- Draft GST Return Rules

- Draft GST Payment Rules

- Draft GST Invoice Rules

- Draft GST Refund Rules

- Draft GST Registration Format

- Draft GST Return Format

- Draft GST Payment Format

- Draft GST Invoice Format

- Draft GST Refund Format